Founders obsess over valuation but ignore the terms that actually decide who gets paid. Here is the math on how a standard clause can cost you $16M on exit. A $100M exit can result in $0 for founders if this clause is wrong.

TL;DR: Liquidation preference determines the payout order when your startup sells. It is the multiplier on the investor's money (1x, 2x) and the participation status (Participating vs Non-Participating) that dictates if they get paid before you or alongside you.

Benchmark: Aim for 1x Non-Participating. This is considered the standard for clean Series A deals by organizations like Y Combinator.

Rule: Be cautious about "Participating" preferred stock. The National Venture Capital Association (NVCA) model term sheet treats it as a negotiated point.

Warning: As our math below shows, a 2x Participating liquidation preference can wipe out 40% of expected founder returns even in a successful exit.

Core Definitions

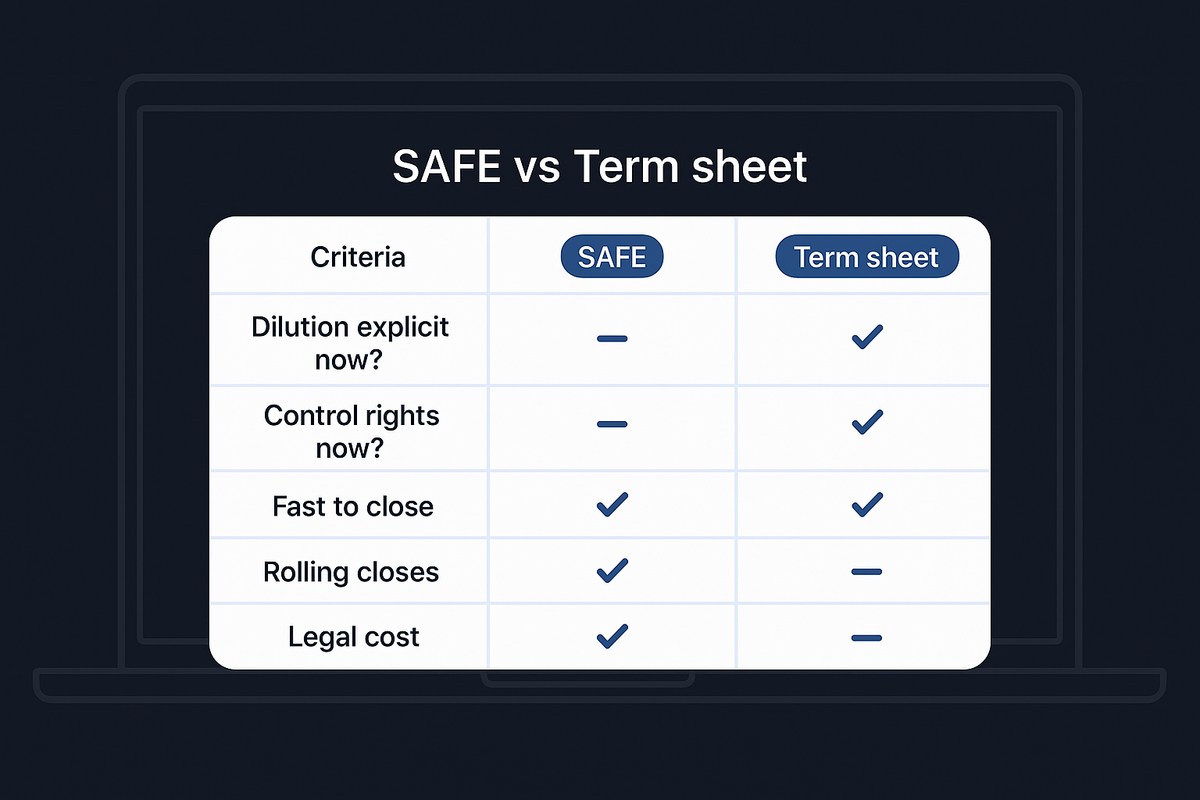

Liquidation Preference: The safety net multiplier. A 1x preference means investors get their original investment back before common shareholders (founders) see a dime. To understand how this compares to early stage funding, see our guide on Term Sheet vs SAFE.

Non-Participating: The investor must choose: take their preference money and run, OR convert to common shares and split the pot. They cannot do both.

Participating: The double dip. Investors get their preference money back first, AND then they get to split the remaining pot with common shareholders.

Seniority: The order of payouts. Standard is usually pari passu (everyone equal) or stacked by round (Series B gets paid before Series A).

Payout Scenarios (The Math)

This comparison models two payout scenarios on a $50,000,000 exit.

Assumptions:

Investment: $10M raised.

Ownership: Investors own 20% fully diluted; Founders own 80%. (You can model your own equity splits with our Option Pool Calculator).

The Trap: Comparing a clean term sheet vs. a shark term sheet.

Payout Metric | Scenario A: 1x Non-Participating (Clean) | Scenario B: 2x Participating (Dirty) |

|---|---|---|

Step 1: Preference Payout | $10,000,000 (Investor takes 1x) | $20,000,000 (Investor takes 2x) |

Remaining to Distribute | $40,000,000 | $30,000,000 |

Step 2: Participation | N/A (Investor already paid) | Investor takes 20% of remaining ($6M) |

Total Investor Payout | $10,000,000 | $26,000,000 |

Total Founder Payout | $40,000,000 | $24,000,000 |

Founder Share of Exit | 80% | 48% |

Sample math:

In Scenario A (Non-Participating), the investor compares their preference ($10M) to their ownership value (20% of $50M = $10M). Since they are equal, the payout is $10M. The remaining $40M flows to founders.

In Scenario B (Participating), the investor takes 2x their money off the top ($20M). They then dip into the remaining $30M for their 20% share ($6M). They turn a $10M check into $26M, leaving founders with significantly less.

Conclusion: The Valuation Trap

Mastering the math of liquidation preference is a necessary step for defense. You can negotiate a high valuation, but if you ignore the preference terms, you risk signing away your exit payout. If you are debating early funding structures, review our SAFE vs Convertible Note breakdown to keep things simple.

Valuation is vanity; liquidation preference dictates the exit. The next time you receive a term sheet, model the exact payout scenarios before signing. Consider the strategic tradeoff of accepting a lower valuation if it means securing a clean 1x non-participating preference, rather than taking a term sheet that could leave you with nothing on a decent exit.

FAQ

What is the difference between participating and non-participating liquidation preference?

Non-participating forces the investor to choose between their guaranteed return (preference) OR their share of the company. Participating allows them to take the guaranteed return AND their share of the remaining proceeds. Participating is much worse for founders.

Does a 1x liquidation preference affect me if I sell for a huge profit?

Generally, no. If you sell for a high multiple, investors with a 1x Non-Participating preference will simply convert their shares to common stock to get their percentage of the deal, as that amount will be higher than their original investment.